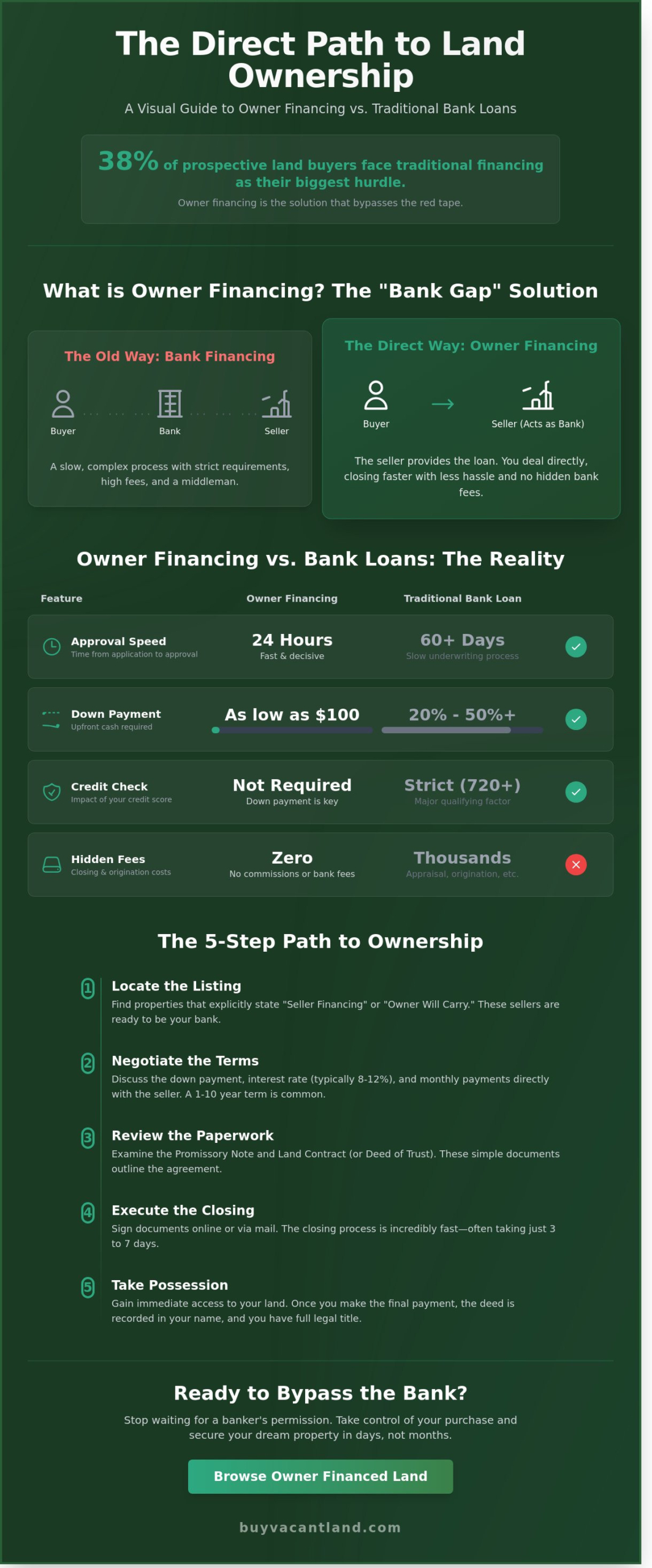

Why waste months begging a bank for a loan when you can secure your dream property in under 72 hours? Data from the 2024 Land Market Survey shows that traditional financing remains the biggest hurdle for 38% of prospective buyers. You shouldn’t have to deal with endless paperwork or massive down payments just to own a piece of dirt. Finding owner financed land is the fastest way to bypass the red tape and start building your future today.

You already know that the traditional mortgage process is broken. It’s slow, expensive, and designed to keep you on the sidelines. This guide shows you how to take control of your purchase with seller-direct terms. You’ll learn how to lock in low entry costs and close your deal without a single bank interview. We’ll break down the exact five-step process to find, negotiate, and secure your property with zero hidden fees. It’s time to stop waiting for a banker’s permission and start your ownership journey now.

Key Takeaways

- Bypass bank red tape and deal directly with the seller for a faster, simpler closing.

- Secure your property using owner financed land agreements that skip strict credit checks and high down payments.

- Compare upfront costs to see why seller financing is the most efficient path to land ownership.

- Master the essential due diligence steps to verify legal access and zoning before you sign.

- Access a national marketplace to find bank-free deals instantly with simple search filters.

What is Owner Financed Land and Why Does it Exist?

Owner financing is a direct real estate agreement where the seller acts as the bank. Instead of visiting a local branch to beg for a loan, you negotiate terms directly with the person who owns the property. You can learn more about the mechanics of What is Owner Financing to understand how these private notes function. This setup bypasses the red tape that usually kills land deals. You make a down payment, sign a contract, and pay the seller in monthly installments until the land is yours.

The “Bank Gap” is the primary reason this market thrives. Traditional lenders rarely fund raw, undeveloped land parcels because they can’t easily value the collateral. In 2023, many major banks required down payments of 50% or more for vacant lots, if they offered a loan at all. Sellers fill this void. They offer owner financed land to buyers who want to bypass these rigid institutional hurdles. It turns a difficult-to-finance asset into an accessible opportunity.

Buyers choose this path for speed and simplicity. You don’t need a perfect credit score to qualify. Most deals feature low down payments and a closing process that takes days rather than months. Sellers also gain a massive advantage. They sell their property faster, create a stream of passive income, and attract a much wider pool of potential buyers. It’s a pragmatic solution for a specialized market. If you want to search for listings close to home, our guide to finding owner financed land near me walks you through exactly how to locate bank-free deals in your area.

The Core Difference: Seller vs. Bank

Banks focus on your credit score and debt-to-income ratio. Sellers focus on the land itself and your ability to make the down payment. This shift in priority changes everything. You eliminate the middleman entirely. This makes zero commissions and zero hidden fees a reality for most transactions. You skip the bank’s appraisal fees and loan origination costs. The process offers immediate emotional relief through a guaranteed approval system that values your time.

Is Owner Financing Legal and Safe?

This is a standard, legally recognized real estate practice used daily across the country. Safety comes from transparency. You should always use recorded documents and reputable title companies to ensure the chain of title is clean. These professionals handle the escrow and verify that the property is free of undisclosed liens. A Land Contract is the primary legal instrument that defines the payment schedule and the eventual transfer of the deed to the buyer.

How Owner Financing Works: A 5-Step Breakdown

Buying owner financed land skips the bank and puts you in control. The process is fast, transparent, and eliminates the typical 60-day wait for a mortgage. You deal directly with the property owner to reach an agreement that fits your budget. Follow these five steps to secure your property today.

- Step 1: Locate the listing. Find a property that explicitly states “Seller Financing” or “Owner Financed” terms. These sellers are ready to act as the bank.

- Step 2: Negotiate the terms. Discuss the down payment and monthly installments directly with the seller. You don’t need a high credit score to qualify.

- Step 3: Review the paperwork. Examine the Promissory Note and either a Land Contract or a Deed of Trust. These documents define your rights and responsibilities.

- Step 4: Execute the closing. Sign the documents using a simple online portal or a mail-away process. This removes the need for expensive in-person meetings.

- Step 5: Take possession. You gain immediate access to the land while making your scheduled payments. You can start planning your build or using the land for recreation right away.

Understanding the Down Payment and Terms

Traditional lenders often demand 20% to 35% down for vacant land. Owner financing is much more accessible. Many sellers accept down payments as low as $100 to $500. Interest rates for owner financed land typically range from 8% to 12%. While this is higher than a standard home mortgage, it eliminates the thousands of dollars in bank fees and loan origination costs. Most land contracts run for a duration of 1 to 10 years. This short term ensures you own the land outright in a fraction of the time of a 30-year mortgage.

The Closing Process: Speed and Simplicity

Bank-funded transactions involve appraisals, inspections, and weeks of underwriting. Owner financing closes in as little as 3 to 7 days. You typically use a Contract for Deed to secure your equitable interest in the property. This document proves you are the buyer and have the right to use the land. You must verify all terms to avoid the dangers of predatory agreements that can occur with unverified sellers. Once you make the final payment, the seller records a Warranty Deed in your name. This transfers full legal title to you forever. If you want a simple path to ownership, you can browse our available properties to find your next investment.

Owner Financing vs. Traditional Bank Loans: The Reality

Banks make land buying difficult. Most traditional lenders require a credit score above 720 and two years of stable tax returns. They reject nearly 20% of land loan applications for minor paperwork errors. Sellers operate differently. When you buy owner financed land, the seller is the bank. They care about your down payment, not your debt-to-income ratio. Approval often happens in 24 hours rather than 60 days. This speed allows you to secure a property before a competitor outbids you.

Upfront costs represent the biggest barrier to entry. Traditional banks demand 20% to 50% down for raw land because they view it as a high-risk investment. On a $50,000 parcel, you need $25,000 cash just to start. Private sellers frequently accept 5% or 10% down. Some even offer low flat-fee down payments of $500 or $1,000. You keep more cash in your pocket to actually develop the property.

The total cost involves a trade-off. You will likely pay a higher interest rate with a seller, often between 8% and 12%, compared to bank rates of 6% to 8%. However, you avoid thousands in bank fees. Banks charge for originations, appraisals, and processing. These “junk fees” can exceed $3,000 on a small loan. With a seller, you skip the red tape and build equity faster through a simplified payment structure. Understanding how seller financing is structured helps you see that the lack of closing costs often offsets the higher interest rate over the first five years.

Possession is the final decider. Banks often place restrictions on how you use the land until the loan is paid or a permanent structure is built. Sellers generally grant immediate use. You can park your RV, clear brush, or start your garden the day you sign the contract. This freedom is essential for those who want to live on their terms right now.

When to Choose Owner Financing

- Non-traditional income: Perfect for the 10% of Americans who are self-employed and struggle with bank documentation.

- Off-grid pioneers: Ideal if you need to move onto the land immediately to start a homestead project.

- Portfolio builders: Great for investors who want to control multiple properties with low initial capital.

Potential Risks and How to Avoid Them

Seller default is a real risk. If the seller still has a mortgage and stops paying, the bank could foreclose on your owner financed land. Protect yourself by requiring a title search and buying title insurance. This ensures the land is free of liens before you sign. Watch out for balloon payments. These are large lump sums due at the end of a 3 or 5-year term. Read the fine print to ensure you can refinance or pay the balance when that date arrives. Always record your contract with the county clerk to establish your legal interest in the property.

Due Diligence: What to Verify Before You Buy

Don’t skip the homework. Buying owner financed land requires a sharp eye for detail. Start with legal access. Ensure the property has a deeded easement or direct road frontage. Landlocked property is a liability, not an asset. You cannot rely on a handshake deal with a neighbor for a driveway. If the access isn’t in writing on the deed, the property has limited value.

Next, verify zoning laws. Contact the county planning department directly. Ask if the land allows for your specific use. Some zones prohibit full-time RV living or mobile homes. In 2023, 15% of rural land buyers discovered zoning restrictions only after closing. Avoid this mistake by getting the permitted uses in writing from local officials. Don’t take a seller’s word for what you can build.

Confirm title clarity. The seller must legally own the land they are financing. Request a title commitment or use a third-party escrow service to verify the chain of ownership. This step protects you from hidden liens or ownership disputes. Check utility availability too. Bringing power to a remote lot often costs between $5,000 and $15,000 per pole if the line isn’t at the road. In 2024, some rural water tap fees have exceeded $3,500. Call the local utility co-op for a specific quote before you sign any contract.

The Essential Land Buyer’s Checklist

- Check for back taxes: Search county records for unpaid property taxes or HOA dues. Unpaid debts can lead to foreclosure even after you start your monthly payments.

- Verify unrestricted status: Look for “unrestricted land” if you want maximum freedom. This means the property has no private covenants, although you must still follow basic county building codes.

- Get a survey: A professional property survey is the only way to guarantee you are standing on the dirt you actually bought.

Negotiating the Best Terms

You have more leverage than you think when purchasing owner financed land. Offer a higher down payment to secure a lower interest rate. If you put 20% down instead of 10%, many sellers will drop the rate by 1% or 2%. This saves you thousands of dollars over the life of the loan.

Ensure the contract includes an early payoff clause with zero penalties. This allows you to refinance with a bank or pay off the balance early without extra fees. Finally, request a 10 or 15 day grace period for monthly payments. This provides a necessary safety net for your credit and peace of mind. Always keep your terms simple and transparent.

Ready to find your next investment? Get your fair cash offer and start your journey today.

Find Your Property on the BuyVacantLand.com Marketplace

BuyVacantLand.com serves as the premier national hub for buyers seeking owner financed land. We cut through the noise of traditional real estate by focusing exclusively on land. You don’t need to deal with the red tape of big banks or the slow pace of traditional lenders. Our platform provides a direct path to property ownership. Use the ‘Owner Financing’ filter on our marketplace to see bank-free deals instantly. This tool saves you hours of manual searching by highlighting sellers who offer their own terms.

We believe in a direct and pragmatic approach. When you find a property you like, you connect directly with the seller. This eliminates middleman delays and removes the 6% commission fees often found in standard transactions. You get clear answers and fast decisions. Our platform is built for efficiency. We value your time and prioritize a no-nonsense experience. You can browse listings across all 50 states and find the exact parcel that meets your needs without the typical stress of property buying.

Why Use a Specialized Land Marketplace?

Traditional real estate sites focus on houses, kitchens, and suburban neighborhoods. We focus 100% on vacant land parcels. This specialization means our tools are designed for the unique needs of land buyers. You get access to cheap land and off-grid opportunities that never hit the MLS. Our streamlined interface allows for fast discovery and quick action. You won’t find distracting residential listings here.

- Zero fluff: Our listings provide the data you need like acreage, zoning, and access.

- Off-grid focus: We specialize in rural parcels that traditional brokers often ignore.

- Direct access: You speak to decision-makers, not assistants or gatekeepers.

- Speed: Our platform is optimized for users who want to move from search to contract in days.

Take the First Step Toward Ownership

Ownership is closer than you think. Don’t let a lack of bank financing stop you from securing your future. Browse our current listings to see what’s available across the United States right now. Every listing is an opportunity to build equity on your own terms. We make the process transparent and accessible for everyone. Whether you want a weekend retreat or a long-term investment, the right parcel is waiting.

Remember that a fair cash offer and simple terms are just a click away. You can find specific land for sale owner financing that fits your monthly budget today. Our system is designed to provide relief and peace of mind through guaranteed transactions. Stop waiting for the perfect moment. Start your search now and secure your owner financed land before someone else takes the opportunity. The process is simple, the terms are clear, and the land is yours for the taking.

Secure Your Property Without the Bank

Traditional bank loans for vacant land typically require down payments between 20% and 50%. They also involve a 30 to 45 day closing period. You can avoid these hurdles by purchasing owner financed land directly from the seller. This 2026 guide highlights how skipping the bank saves you time. It eliminates the need for perfect credit. You’ve learned how to verify titles and use a 5 step process to ensure a secure transaction. Real estate is simple when you use a pragmatic approach.

BuyVacantLand.com is a specialized vacant land marketplace. We offer national coverage across the United States. We create direct seller to buyer connections to remove the typical red tape. Our system prioritizes efficiency and reliability. You close your deal fast. Don’t let institutional requirements stand in the way of your investment goals. You can find your next property on our streamlined platform right now.

Browse Owner Financed Land Listings Now

Get started today and experience the relief of a simple, bank-free purchase.

Frequently Asked Questions

Is owner financing the same as rent-to-own for land?

No, owner financing and rent-to-own are different legal structures. Owner financing involves a direct sale where the seller acts as the bank. You gain equitable title immediately. Rent-to-own is a lease agreement where you pay rent plus a premium for the future right to buy. If you are searching for rent to own land near me as an alternative path to ownership, understanding how lease-purchase contracts differ from a standard land contract is essential before you sign. Most buyers prefer owner financing because it secures your interest in the property from day one.

Can I build a house on land while I am still paying the seller?

You can usually build on owner financed land if your contract explicitly allows it. Most sellers require you to obtain all necessary county permits and follow local building codes. Some agreements may restrict major construction until you reach 20 percent equity to protect the seller’s collateral. Always review your specific contract terms before you break ground or clear trees on the property.

Do I need a high credit score to qualify for owner financing?

You don’t need a high credit score to qualify for this type of land purchase. Sellers focus on your down payment and ability to make monthly installments rather than a rigid FICO score. This makes land ownership accessible even if you have a thin credit file or past financial setbacks. A typical down payment of 10 to 20 percent is usually enough to secure the deal. Buyers who want to explore local options can use our owner financed land near me guide to find qualifying properties in their region without a credit check.

What happens if I stop making payments on an owner-financed property?

You risk losing the property and all previous payments if you stop making payments. The seller can initiate a forfeiture or foreclosure process depending on your state laws. In a standard Land Contract, the seller may reclaim the property in as little as 30 to 60 days after a missed payment. Always communicate with the seller early to avoid losing your investment and your equity.

Are there hidden fees in a land contract?

There are no hidden fees if you use a transparent contract. You should only see the purchase price, interest rate, and standard closing costs. Watch for specific clauses regarding late payment penalties or loan servicing fees which can add 15 to 50 dollars to your monthly bill. We believe in zero hidden commissions and zero surprise charges to keep your transaction simple and fast.

How do I make sure the seller actually owns the land?

Verify ownership by conducting a professional title search through a licensed title company. This process confirms the seller holds a clear title and identifies any existing liens or encumbrances. According to the American Land Title Association, title insurance protects you from claims against your ownership. Never send a down payment until you see a recorded deed or a title commitment in the seller’s name.

Can I pay off my land contract early?

You can pay off your owner financed land early in most cases. Check your contract for a prepayment penalty clause. Most private sellers don’t charge these fees because they want their cash faster. Paying early saves you thousands in interest over the life of the loan. It’s a smart move that moves you toward full ownership and a clear title ahead of your original schedule.

Who pays the property taxes during the financing period?

The buyer is typically responsible for property taxes during the financing period. The seller may pay the bill directly and bill you monthly, or you might pay the county tax collector yourself. Check your contract for these specific tax obligations. Failure to pay property taxes can lead to tax liens. This can jeopardize both your interest and the seller’s interest in the vacant land.

Join The Discussion