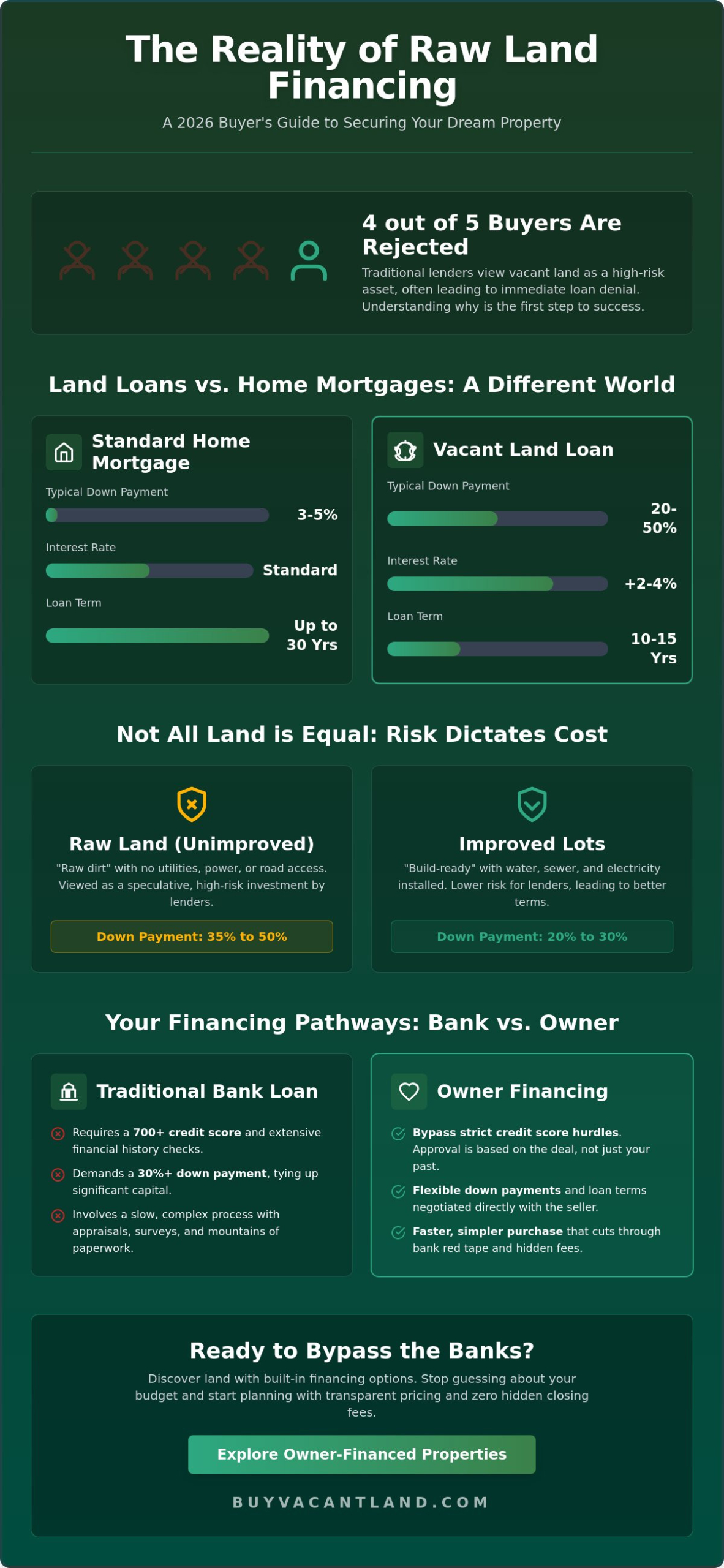

Most buyers treat raw land like a standard home mortgage and get rejected by 4 out of 5 traditional lenders before they even start. It’s a harsh reality. Banks view vacant property as a high-risk asset. This is why they often demand down payments ranging from 35% to 50% of the total purchase price. You likely already feel the frustration of searching for a lender who understands unimproved acreage. It’s confusing. It’s slow. It often leads to dead ends that waste your time and your money.

Stop guessing about your budget. Start planning with facts. Our land loan calculator gives you a direct path to the numbers you need for 2026. We’ll show you exactly how to estimate your monthly payments and master the math of raw land financing. You’ll learn why improved land costs less to finance than raw dirt. We also reveal how to find the best terms for your purchase. This guide covers everything from interest rate trends to owner financing alternatives that cut through the red tape. Let’s get your property purchase moving forward today.

Key Takeaways

- Learn why banks view vacant property as high-risk and how to secure the best possible financing terms.

- Use a land loan calculator to instantly estimate monthly payments and compare shorter loan terms.

- Compare bank loans against owner financing to bypass credit hurdles and speed up your purchase.

- Discover how zoning and road access directly influence your financing costs and interest rates in 2026.

- Simplify your purchase by finding land with built-in financing and zero hidden closing fees.

Understanding the Real Cost of Raw Land Financing

Financing vacant property requires a different strategy than buying a house. A land loan is a specialized financial product designed solely for the acquisition of acreage or lots. Banks classify these loans as high-risk investments. A house provides immediate collateral that a lender can resell quickly. Raw land doesn’t offer that same security. If a borrower walks away, the bank is stuck with a plot of dirt that may have limited market appeal. This risk factor is why you won’t find the same terms offered for a 30-year residential mortgage.

You’ll see a sharp contrast between land financing and traditional home loans. Mortgages are standardized and often subsidized. Land loans are custom and cautious. The math changes based on whether the land is unimproved or improved. Unimproved land is “raw” dirt with no utilities, power, or road access. Improved land is “build-ready” with water, sewer, and electricity already installed at the site. This distinction dictates your interest rate and your total out-of-pocket cost.

Why Land Loans Require Different Math

Lenders lack the security of a physical building to protect their investment. Because of this, interest rates in 2026 typically sit 2% to 4% higher than standard residential rates. You need a clear Amortization calculator to see how these premiums increase your monthly obligation. Since there’s no house to act as a safety net, the lender relies heavily on your credit score and the property’s appraisal. Loan-to-Value (LTV) for raw land is the ratio of the total loan amount divided by the appraised value of the property.

The Role of Down Payments in Land Math

Forget the 3% or 5% down payments common in residential real estate. Land lenders demand significant skin in the game. You’ll typically need a down payment between 20% and 50% to close a deal in 2026. Your intended use of the property dictates this percentage. If you’re building a primary residence immediately, a 20% down payment is often sufficient. If you’re holding the land for future investment, expect to bring 40% or 50% to the closing table.

Using a land loan calculator is essential to determine if your available cash covers both the down payment and the associated closing costs. Cash offers remain the fastest path to ownership. They bypass the strict LTV requirements and high interest rates that banks impose on vacant property. Eliminating the lender also eliminates the stress of appraisals and long wait times. This simplicity is why many buyers prefer a land loan calculator to compare the long-term cost of financing versus the immediate benefits of a cash purchase.

How to Use a Land Loan Calculator for Different Property Types

Using a land loan calculator is the fastest way to see your financial future. Start with the purchase price. Enter your expected interest rate. Most land loans in 2026 carry rates 1% to 3% higher than standard home mortgages. Next, adjust the loan term. Do not expect a 30-year term. Banks usually cap land loans at 10 or 15 years. This shorter window reduces their risk. It also means you pay significantly less interest over the life of the loan.

Include property taxes in your math. Raw land taxes are often less than $500 per year for small parcels, but this varies by county. Set your payment schedule to monthly by default. Some agricultural lenders use annual or semi-annual schedules to match harvest cycles. Verify this with your bank before you finalize your estimate. If the numbers don’t fit your budget, you can always sell your land for cash and avoid the financing headache entirely.

Calculating for Raw Land vs. Improved Lots

Raw land is the most basic property type. It has no utilities. It lacks road access. It has no structures. Lenders view raw land as a speculative investment. This means they often require a 50% down payment. Use the tool to see how a 50% stake changes your monthly obligation compared to a standard home loan.

Improved lots are different. These parcels have water, power, and road access already in place. Because the land is build-ready, lenders feel safer. Your required down payment might drop to 20% or 30%. This infrastructure lowers your upfront cash needs. Always toggle between these percentages in your calculation to see which option fits your available capital.

Calculating for Farm and Ranch Loans

Agricultural loans use different variables. Your payment schedule might follow the money. Quarterly or semi-annual payments are common in this sector. Lenders also look at the land’s income potential. If the dirt produces crops or supports livestock, your approval odds increase. Income-producing land provides a safety net for the bank.

Government backing is a major factor for rural buyers. The USDA Farm Loan Programs offer specific financing for those who qualify. These programs often provide better terms and lower down payments than traditional banks. When using your land loan calculator, check if your property qualifies for these ag-specific rates. It could save you thousands in interest over a 10-year period.

Traditional Bank Loans vs. Owner Financing: A Comparison

Banks and private sellers operate on different planets. A traditional bank loan requires mountain of paperwork. You’ll need a 700+ credit score and a 30% down payment. The bank will demand an appraisal, a survey, and an environmental study. This process takes 45 to 60 days. It’s slow and expensive. Owner financing is the opposite. It’s built for speed. You negotiate directly with the seller. You skip the middleman. You skip the credit bureaucracy.

Most sellers offer owner financing because they want a fast exit. They don’t care about your debt-to-income ratio. They care about your down payment. This bypasses the credit score hurdles that stop most land buyers. You get the land now. You start your project immediately. Buying direct from a seller also secures the zero commission benefit. You don’t pay 6% to an agent. You don’t pay loan origination fees. You don’t pay for points. You keep your cash in your pocket. You can find these deals on vacant land marketplaces by filtering for “seller financing” or “owner carry” tags.

The Math of Owner Financing

Use a land loan calculator to compare these two paths. Owner financing often features a balloon payment. This is a large lump sum due at the end of a short term, usually 3 or 5 years. It keeps your monthly costs low while you prepare for a permanent build. Sellers offer flexible terms that banks won’t touch. You can negotiate the interest rate and the payment schedule. For more details on these bank-free strategies, see our Owner Financed Land guide.

When a Traditional Bank Loan Makes Sense

Banks are for the “bankable” buyer. In 2026, this means you have a credit score above 720 and stable documented income. You’ll get a lower long-term interest rate from a bank. This is a smart move for a 20-year hold. It’s a strategic way of buying land usa if you have the patience for their red tape. Use a land loan calculator to see the total interest cost over the life of the loan. If the bank’s lower rate saves you more than the $5,000 in closing fees you’ll pay upfront, take the bank loan. If you need to move fast, stick with the seller.

- Bank Loans: Best for high credit, long-term holds, and lowest rates.

- Owner Financing: Best for speed, credit challenges, and zero-commission deals.

- Closing Speed: Banks take 60 days; owners take 7 days.

5 Factors That Impact Your Land Loan Interest Rates in 2026

Lenders view land as a speculative investment. Higher risk for them means higher interest rates for you. You can’t control the economy, but you can control which property you buy. In 2026, banks look for stability and clear exit strategies. If your land is hard to sell, your rate will climb. Use a land loan calculator to see how even a 0.5% rate increase changes your total interest paid over 10 years.

Five specific variables dictate your final loan terms:

- Property Location and Accessibility: Road frontage is essential. Landlocked parcels are nearly impossible to finance. If a lender can’t drive a truck to the property, they won’t fund the deal.

- Buyer Creditworthiness: Your debt-to-income (DTI) ratio must stay below 43% for most traditional land loans. A credit score above 720 secures the best available market rates.

- Lender Type: Local credit unions often offer better rates on small lots because they know the local market. National ag-lenders specialize in large farm tracts but require higher down payments.

- Zoning Classifications: Residential zoning is the safest bet for banks. Commercial or industrial land requires specialized appraisals and higher rates.

- Infrastructure Status: Land with existing power and water is “shovel-ready.” Lenders reward this readiness with lower interest.

Zoning and Its Financial Impact

Zoning tells the lender what the land is worth if you stop paying. Residential lots are easy to value because of nearby comparable sales. Industrial parcels involve environmental risks and complex regulations, which drive up interest rates. Many buyers seek “unrestricted land” for freedom, but this lack of oversight often scares traditional banks. Lenders want predictable outcomes. You must provide a professional land survey before loan finalization to confirm boundaries and easements. Without a survey, the bank won’t close the deal.

The Infrastructure Variable

Raw land requires a massive capital injection to become usable. Bringing in utilities can cost between $10,000 and $30,000 depending on the distance to the main line. If the property already has a functioning well or septic system, the lender views these as tangible assets. They act as additional collateral. This reduces the bank’s risk and can lower your rate. For example, land for sale in florida often sees drastic price and rate fluctuations based on whether the lot is in a developed “grid” or a remote rural area. Always verify utility proximity before you run your numbers through a land loan calculator.

Stop worrying about bank approvals and high interest rates. Get your fair cash offer and sell your land fast without the financing headaches.

Bypassing the Bank: Finding Land with Built-in Financing

Traditional banks make raw land loans difficult in 2026. They often demand 35% to 50% down payments. They require exhaustive paperwork and perfect credit scores that many buyers simply don’t want to deal with. BuyVacantLand.com offers a faster, more efficient path. You skip the middleman and find properties with flexible terms directly from the source. This platform simplifies your search for cheap land for sale by connecting you with sellers who provide their own financing. You avoid the stress of bank approvals and get straight to the closing table. The process is built for speed and reliability.

Why a Marketplace Beats a Bank for Raw Land

Banks often view vacant land as a high-risk investment. This perspective leads to high interest rates and restrictive repayment windows. Specialized marketplaces provide access to off-market feeling deals that never reach the traditional MLS. You communicate directly with the seller to establish financing terms that work for your budget. This direct approach removes the bureaucratic red tape. You can expect a streamlined experience with zero commissions and zero hidden fees. Consider these advantages:

- Zero loan origination fees: Sellers don’t charge the points and processing fees that banks do.

- Flexible down payments: Many sellers accept much less than the standard 35% required by commercial lenders.

- No credit impact: Most owner-financing deals don’t require a hard credit pull, keeping your score intact.

By filtering for owner-financed listings, you eliminate the guesswork from your land loan calculator results. You see the exact terms upfront. This transparency ensures you never waste time on a property you can’t afford. You get a simple, guaranteed transaction without the bank’s interference.

Ready to Run the Numbers?

Before you sign a land purchase agreement, complete a final check. Verify the 2026 property tax rates. Confirm the legal access to the lot. Check for any local building moratoriums. Once you have these facts, use our land loan calculator to see how a specific property fits your monthly cash flow. Testing real-world numbers against actual listings gives you immediate clarity. You aren’t just guessing; you’re making a calculated investment.

BuyVacantLand.com follows a strict logical progression to get you results: identify the lot you want, run the numbers, and secure the deal. Set up alerts for new vacant land listings to stay ahead of the market. The best deals often sell within 48 hours. Don’t let a low-down-payment opportunity pass you by. Take control of your property search today.

Secure Your 2026 Land Investment Now

Smart land ownership requires precise financial planning. Use a land loan calculator to determine your exact monthly costs and compare traditional bank loans against owner financing. Industry standards for 2026 indicate that most lenders require down payments between 30% and 50% for raw acreage. You can bypass these high entry barriers by choosing properties with built-in financing. This approach eliminates traditional bank delays and puts you in control of the transaction immediately.

Our platform simplifies your search by offering a specialized marketplace for raw and undeveloped lots. You get direct-to-seller communication and a transparent process from start to finish. We focus on efficiency so you can avoid the stress of typical real estate transactions. Forget about high commissions or hidden fees. We keep the process simple with zero surprises and zero red tape. You deserve a straightforward path to property ownership that respects your time and your budget.

Find Your Next Investment on BuyVacantLand.com

The right lot is ready for you to start your next project today.

Frequently Asked Questions

Is it harder to get a loan for land than a house?

Yes, lenders view land as a higher risk because it lacks a physical structure to secure the value. Banks often require 20% to 50% down for these transactions. Vacant land doesn’t generate immediate income or provide shelter, so default rates are historically higher. You’ll need a solid development plan and a high credit score to get approval from traditional financial institutions.

What is a typical down payment for a land loan in 2026?

Expect to pay between 20% and 50% of the purchase price as a down payment in 2026. Raw land usually requires a 50% down payment because it has no utilities or road access. Improved land with infrastructure might only need 20% to 30%. Use a land loan calculator to see how these specific percentages impact your monthly cash flow and total interest costs.

Can I use a land loan calculator for owner-financed property?

You can use a land loan calculator for owner-financed deals by entering the specific interest rate and term agreed upon with the seller. Owner financing often skips the bank’s strict rules, but the interest rates usually range from 5% to 10%. This tool helps you compare the seller’s terms against traditional bank financing options to ensure you’re getting a fair deal without hidden costs.

Does the 2026 interest rate for land differ from home mortgage rates?

Land loan interest rates are typically 1% to 3% higher than standard 30-year residential mortgage rates. Financial institutions charge more to offset the increased risk of lending on undeveloped dirt. According to 2024 Federal Reserve data trends, land rates remain elevated compared to home loans. You’ll see these higher rates reflected in your total financing costs when you run your final numbers.

Can I get a land loan with a 600 credit score?

Securing a land loan with a 600 credit score is difficult, as most lenders require a minimum score of 680 to 720. Some specialized lenders or local credit unions might accept lower scores if you provide a 40% down payment. Your interest rate will be significantly higher at this credit level. Focus on improving your score to 700 to access better terms and lower fees.

What happens if I want to build a house on the land later?

You’ll likely need to refinance your land loan into a construction loan when you’re ready to build. Construction loans cover both the land cost and the build expenses. Once the house is finished, the loan converts into a permanent mortgage. This process streamlines your debt into one monthly payment and requires a new appraisal based on the 2026 market value of your blueprints.

Are there special calculators for USDA land loans?

Specialized calculators exist for the USDA Rural Development programs, specifically for Section 523 and 524 loans. These loans are for low-to-moderate income applicants in rural areas. They have specific requirements for site development and building timelines. Use a dedicated USDA tool to account for their unique 2% guarantee fee and specific eligibility criteria based on your 2026 household income levels.

How do I calculate property taxes on vacant land?

Multiply the assessed value of the land by the local millage rate provided by the county tax assessor. Vacant land is usually taxed at a lower rate than improved property. Check the county’s public records for the 2025 assessment data to get an accurate baseline. If the millage rate is 1.5%, you’ll pay $15 for every $1,000 of assessed value annually.

Join The Discussion