Did you know that closing costs for vacant land often reach 5% of the purchase price before you even factor in commissions? Most buyers assume empty lots mean empty fee schedules. You want a clear path to ownership without the stress of hidden charges appearing at the last minute. It’s frustrating to find a perfect lot only to realize your budget didn’t account for a $2,300 survey or a $1,500 appraisal fee. You need a simple way to track these expenses before they derail your deal.

You deserve a transaction that’s fast, transparent, and free of surprises. This guide ensures you understand every fee, tax, and professional charge involved in a land transaction so you can budget with total certainty. We’ll break down the specific costs for 2026, from title insurance premiums to state transfer taxes. You’ll learn which fees are negotiable and how to build a percentage-based budget that actually works. Follow this sequence to eliminate confusion and secure your property with total financial confidence.

Key Takeaways

- Calculate a precise budget of 2% to 5% to cover all closing costs for vacant land without last-minute financial surprises.

- Identify mandatory due diligence fees, including professional surveys and title insurance, to secure your property rights effectively.

- Master negotiation tactics for fee splits and closing credits to reduce your total out-of-pocket expenses at the signing table.

- Minimize your final bill by shopping for independent title companies and bundling technical services like soil and percolation tests.

What Are Closing Costs for Vacant Land?

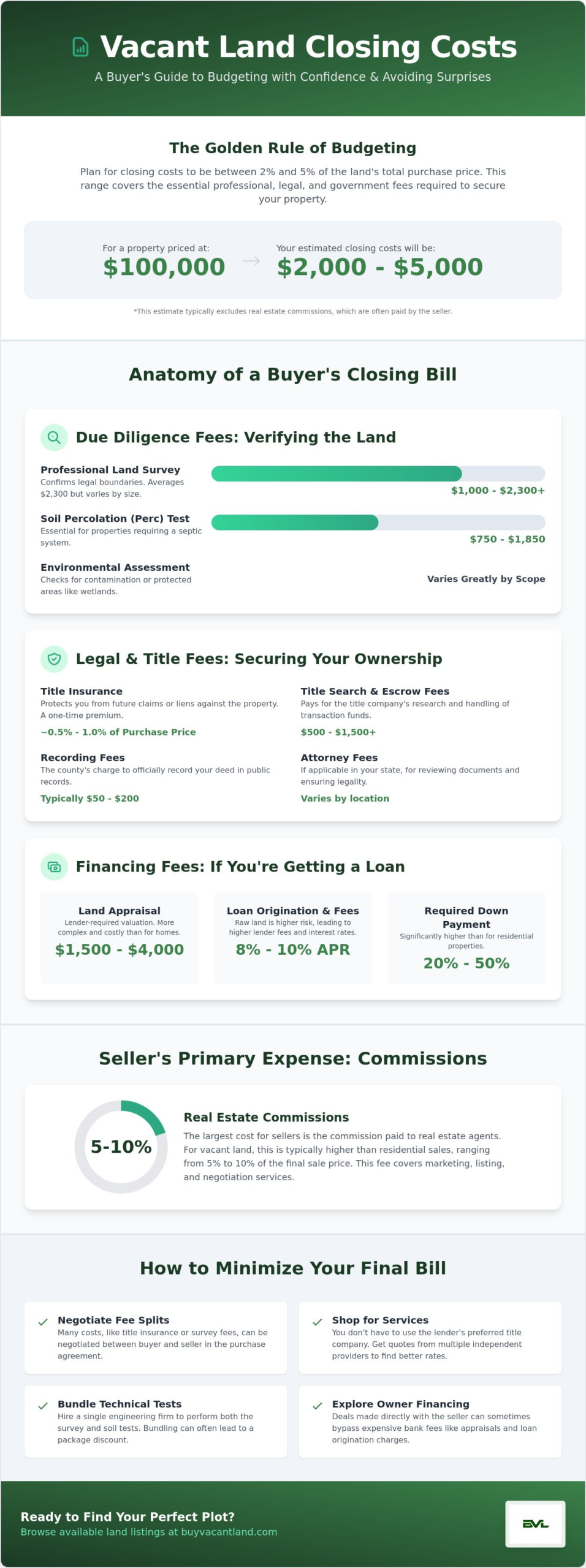

Closing costs are the final bundle of fees you pay to transfer a property title. These charges represent the professional and administrative labor required to ensure your ownership is legally sound. Understanding What Are Closing Costs for Vacant Land? is the first step toward a successful purchase. You must budget for these expenses early. In a typical transaction, closing costs for vacant land range from 2% to 5% of the total purchase price. This percentage covers a variety of specific charges.

Professional services make up a large portion of your bill. You’ll pay for experts to verify the land’s condition and legal boundaries. Government taxes and administrative processing fees add to the total. These aren’t optional “add-ons” for your purchase. They’re essential components of a secure transaction. Skipping these steps can lead to expensive legal battles or unusable property later. Focus on these three main categories:

- Professional Fees: Payments for surveyors, attorneys, and environmental engineers.

- Government Charges: Recording fees and state transfer taxes.

- Administrative Costs: Escrow fees and title search expenses.

The Lifecycle of a Land Closing

The process moves fast once you find a lot you like. First, you open escrow and deposit your earnest money. This shows the seller you’re serious. Then, you enter the due diligence period. This is the most active phase. You’ll hire professionals to conduct soil tests and boundary surveys. Most of your out-of-pocket costs occur during this window. Finally, you reach the signing stage. You’ll finalize the paperwork and pay the remaining balance. The process ends when the county records your new deed, officially making you the owner.

Why Vacant Land Costs Differ from Residential

Land transactions have a different focus than home sales. You don’t need to pay for roof inspections or termite reports. Instead, your money goes toward verifying the ground itself. You’ll spend more on environmental assessments and soil percolation tests. These confirm the land can support a septic system or a foundation. Title searches for raw land are often simpler. There are usually fewer previous owners and no building liens to track. This simplicity can result in lower title insurance premiums compared to improved properties. You aren’t insuring a structure, so the risk profile is lower for the insurer. This helps keep your total closing costs for vacant land manageable if you plan correctly.

Common Buyer Expenses: Due Diligence and Financing

Buyers carry the heaviest load during the closing process. You aren’t just paying for the dirt; you’re paying for the certainty that the dirt is yours and usable. Title insurance is your first line of defense. It protects your ownership against future legal claims or hidden liens. While title insurance costs can vary, a $100,000 policy might typically cost around $780 as of March 2026. If your purchase price is $250,000, expect that premium to rise to approximately $1,521. These closing costs for vacant land are non-negotiable for anyone seeking peace of mind.

Professional surveys are equally critical. You can’t rely on old maps or handshake agreements. A modern land survey averages $2,300 nationally. For a small lot under one acre, you might pay less than $1,000. However, larger or complex parcels can easily reach $1,500 or more. You also need to budget for recording fees. The county clerk charges these to update public records and finalize your deed. These administrative fees are usually small but essential for a legal transfer.

Essential Due Diligence Costs

Due diligence is where land buyers often stumble. You must verify the land’s physical capabilities before the deal closes. A soil percolation (perc) test is mandatory if you plan to build. This test determines if the ground can support a septic system. Expect to pay between $750 and $1,850 for this service. You might also need environmental assessments to check for protected wetlands or past contamination. These steps are vital for understanding how do you buy land without overpaying for unusable property. If you’re looking for verified parcels to start your search, you can browse available land listings today.

Financing Fees and Appraisals

Financing vacant land is more expensive than buying a home. Lenders view raw land as a higher risk. This risk reflects in your loan origination fees and interest rates, which currently range from 8% to 10%. Land appraisals also cost more than residential ones. A professional land appraisal typically costs between $1,500 and $4,000. This higher price is due to the complexity of finding comparable sales for undeveloped lots. You can manage some of these closing costs for vacant land by exploring owner financed land options. These deals often bypass strict bank requirements and high origination fees. Keep in mind that your credit score still impacts your final fee schedule and down payment requirements, which often fall between 20% and 50%.

Seller Closing Costs: Commissions and Transfer Fees

Sellers face a different set of financial burdens during the final transfer. While buyers handle the due diligence, you must cover the costs of marketing and legal clearance. Real estate commissions represent your largest expense. For land, these typically range from 5% to 10% of the sale price. This is higher than residential home commissions because land often requires more time and specialized marketing to find the right buyer. Following recent industry shifts, these rates are more negotiable than ever. Some sellers now achieve total commissions in the 4% to 5% range by negotiating aggressively.

Transfer taxes are another mandatory deduction in many states. These are taxes triggered by the act of selling the asset. If you sell land in Florida, you’ll pay a documentary stamp tax of $0.70 per $100 of the sale price. However, sixteen states currently charge no state-level transfer tax. These include Alaska, Arizona, Colorado, Idaho, Indiana, Kansas, Louisiana, Mississippi, Missouri, Montana, New Mexico, North Dakota, Oregon, Texas, Utah, and Wyoming. You must also pay prorated property taxes. This ensures you only pay for the days you actually owned the property during the current tax year. These closing costs for vacant land are deducted directly from your proceeds at the signing table.

Marketing and Listing Expenses

Effective marketing requires an upfront investment or a deduction from your final payout. High-quality drone footage and professional photography are standard for modern listings. These tools help buyers visualize the terrain and access points from anywhere in the country. When listing cheap land for sale, you might find more flexible commission structures, but administrative fees remain. You must also account for the cost of preparing Seller Disclosure documents. These forms protect you from future liability by detailing everything you know about the property’s history and condition. Accuracy here prevents legal disputes after the sale.

Clearing the Title for a Smooth Sale

You cannot sell what you do not clearly own. Sellers are responsible for resolving “clouds” on the title before the transaction completes. This includes paying off old liens, resolving boundary disputes, or fixing errors in previous deeds. If your property benefited from agricultural or timber tax deferrals, be prepared for “rollback taxes.” These are back taxes triggered when the land’s use changes or it transfers to a new owner. Finally, hire a professional to draft a clean Warranty Deed. In at least 20 “attorney states,” a licensed lawyer must supervise the closing. This legal representation usually costs between $500 and $1,500. Taking these steps early prevents your closing costs for vacant land from ballooning due to last-minute legal delays. Clear the path for your buyer to ensure a swift, assured transaction.

Negotiating the Split: Who Pays for What?

Negotiation determines your final out-of-pocket total. Don’t assume the fee split is set in stone. Standard practice usually dictates that buyers pay for due diligence while sellers pay for title clearing. However, every line item is a potential point of discussion. Local customs often drive these splits, so you must understand your state’s specific norms. In some regions, sellers traditionally pay for the title policy. In others, the buyer handles it entirely. Knowing these patterns gives you a baseline for your offer.

Cash buyers hold the most leverage in any transaction. If you offer a cash deal, you can often push more closing costs for vacant land onto the seller. Sellers value the speed and certainty of cash. They might cover the survey or recording fees just to move the asset quickly. If you are financing, you have less room to maneuver. Use closing credits to your advantage instead. A seller can agree to pay a specific dollar amount toward your costs at the table. This reduces your upfront cash requirement without changing your loan amount. It’s a pragmatic way to keep your liquid capital intact.

Strategies for Land Buyers

Be aggressive during the inspection period. Request that the seller pays for a new boundary survey before you sign the final papers. If the survey reveals issues or soil tests show limited buildability, ask for a credit immediately. You can use these findings to justify a lower purchase price or a seller credit for future site preparation. Some buyers choose to cover all closing costs for vacant land in exchange for a significantly lower purchase price. This simplifies the deal for the seller and makes your offer stand out. It’s about finding the balance that secures the property without draining your reserves.

Strategies for Land Sellers

Make your listing irresistible by offering to pay for the title insurance upfront. This small gesture removes a major financial hurdle for the buyer. It projects an aura of reliability and transparency. Set a “Firm” price that already accounts for your anticipated out-of-pocket expenses. This prevents stressful back-and-forth negotiations at the last minute. Using transparent listings on BuyVacantLand.com helps reduce friction from the start. Clear communication about who pays for what leads to a smoother closing process. If you want to see how professional sellers structure their deals, view current land listings to compare market standards and finalize your strategy.

How to Minimize Closing Costs and Close the Deal

Control your expenses by shopping for your own service providers. Don’t use the default title company suggested by an agent. You have the legal right to choose. Request quotes from at least three firms for your title insurance and survey work. Savings of even $200 on a policy add up quickly. Bundling services is another efficient strategy. Hire one engineering firm to handle your boundary survey, soil percolation test, and environmental assessment. This reduces mobilization fees. The crew only makes one trip to the site, which lowers your total closing costs for vacant land.

Review your Closing Disclosure at least 72 hours before the final appointment. This is a legal requirement for most financed deals. It’s your chance to spot clerical errors or hidden fees. Verify every line item against your original estimate. Don’t wait until you’re at the table to ask questions. Accuracy now prevents expensive delays at the signing table. A smooth closing depends on your attention to these details.

Pragmatic Budgeting for Your Land Purchase

Budgeting requires a no-nonsense approach. Create a “worst case” scenario for your transaction. Add a 10% buffer to your total estimate to handle unexpected recording fees or minor legal corrections. Be aware that low-cost lots often have the highest closing costs for vacant land relative to the purchase price. A $5,000 parcel may still require a $1,000 survey and $500 in title fees. This makes the percentage much higher than the standard 5% seen on larger deals. Always verify utility access fees before the closing date. These impact your long-term development budget even if they aren’t part of the immediate transfer.

Taking Action on a National Marketplace

Direct-to-buyer listings eliminate unnecessary middleman markups. Using a specialized marketplace streamlines the transaction. You deal directly with the source. This reduces administrative friction and speeds up the timeline. Prepare your documentation early. Provide your ID, proof of funds, and tax information to the escrow officer immediately. This prevents “rush” fees from service providers who have to work on short notice. Efficiency saves money. It provides peace of mind. Ready to buy or sell? List your vacant land for sale on our national marketplace today.

Master Your Land Closing Today

You now have a clear roadmap for your next transaction. Budgeting a precise percentage of the purchase price ensures you aren’t caught off guard by unexpected fees. Focus on your due diligence. Verify your boundaries with a professional survey and protect your investment with reliable title insurance. These steps transform a complex legal process into a manageable sequence of actions.

Understanding closing costs for vacant land gives you a competitive edge in any market. You can negotiate from a position of strength and close deals much faster. Efficiency is the key to successful asset ownership. Eliminate the stress of the unknown by using a platform built specifically for raw property transactions.

Our specialized marketplace connects owners directly with targeted buyers for raw and undeveloped land. We provide a streamlined listing process with national reach to help you move property quickly. List your vacant land for sale on our national marketplace and take the final step toward a successful sale. You’re ready to move forward with total financial certainty and peace of mind.

Frequently Asked Questions

How much are closing costs on vacant land in 2026?

Expect to pay between 2% and 5% of the total purchase price for your transaction. This percentage covers administrative fees, recording charges, and state-level taxes. On a $50,000 lot, your closing costs for vacant land would typically range from $1,000 to $2,500. Always verify local tax rates as they vary significantly by state and county.

Who typically pays the closing costs on a land sale?

Both parties usually share the financial burden based on local customs and your specific contract. Buyers typically cover due diligence items like soil tests, appraisals, and surveys. Sellers generally pay for real estate commissions and the costs associated with clearing existing liens from the title. You can negotiate these splits during the offer phase to reduce your out-of-pocket cash requirements.

Are closing costs lower for land than for a house?

Total dollar amounts are usually lower because you aren’t paying for structural inspections or high-value homeowners insurance. However, the percentage can be higher on low-cost lots. Professional fees like surveys and appraisals have fixed minimum costs that don’t scale down for cheap land. Budget for these fixed professional charges regardless of the final purchase price.

What is the most expensive part of closing on vacant land?

Real estate commissions are the largest single expense for sellers, often ranging from 5% to 10% of the sale price. For buyers, the most expensive components are usually the professional survey and the land appraisal. A comprehensive survey averages $2,300 nationally. These technical reports are essential for verifying boundaries and securing financing for raw land.

Do I need a lawyer for a land closing?

You must hire a licensed attorney if the property is located in one of the 20 “attorney states” that require legal supervision for real estate transfers. Even in other states, an attorney provides valuable protection for complex deals involving easements or mineral rights. Legal fees for a standard residential land closing typically range from $500 to $1,500.

Can closing costs be rolled into a land loan?

Most lenders require you to pay closing costs for vacant land in cash at the signing table. Land loans already carry higher risks and stricter down payment requirements of 20% to 50%. Attempting to finance closing fees further increases the lender’s exposure. Check with local credit unions or Farm Credit lenders for specific programs that might allow for fee wrapping.

What happens if I find an encroachment during the survey?

Stop the transaction immediately and demand a resolution from the seller. Encroachments, such as a neighbor’s fence or building on your property, create legal “clouds” on the title. The seller must either remove the obstruction or provide a closing credit for the loss of land value. Never ignore these findings as they complicate future sales and construction permits.

Is title insurance mandatory for vacant land?

Lenders always require a title insurance policy to protect their financial interest in the property. If you pay cash, insurance isn’t legally mandatory but remains a critical safeguard against hidden ownership claims or deed errors. One single payment at closing protects your rights for as long as you own the land. It’s a small price for total legal certainty and peace of mind.

Join The Discussion