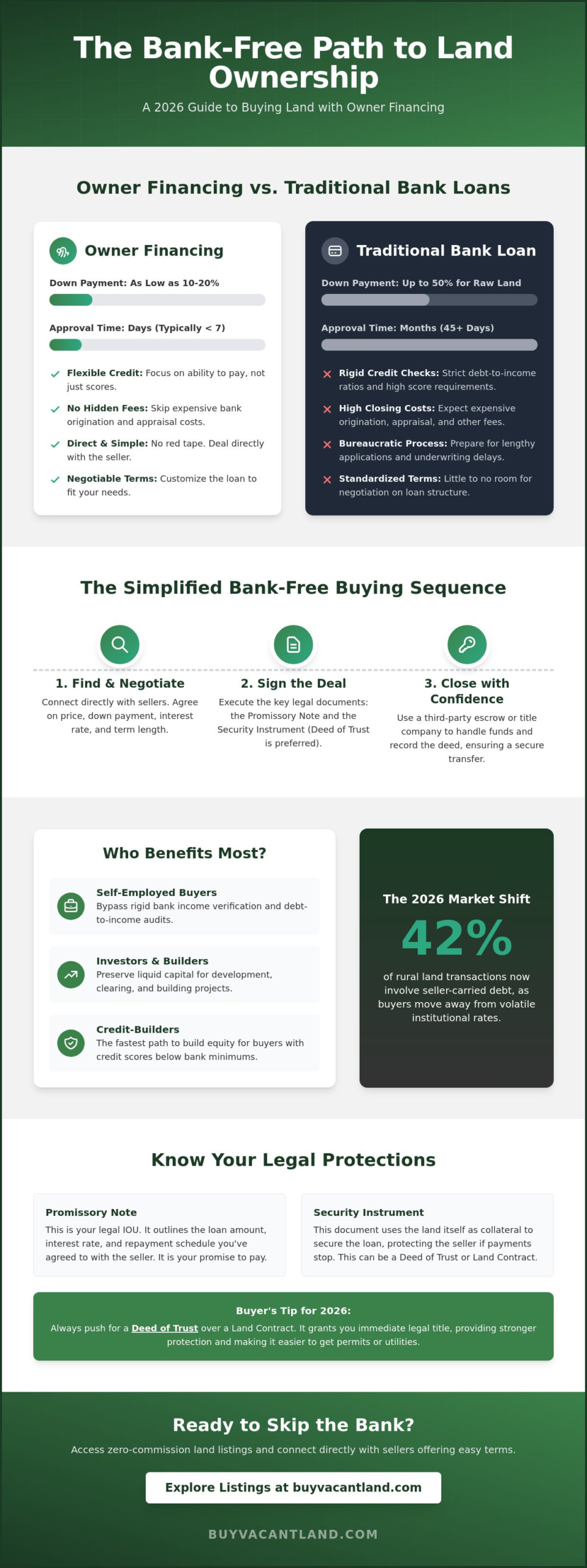

Traditional lenders often demand down payments as high as 50% for raw acreage, effectively locking most buyers out of the market. Why let a bank officer’s rigid credit requirements stand between you and your property? You deserve a faster, simpler path to ownership. You already know that the standard mortgage process is slow and bureaucratic. By choosing land with owner financing, you bypass the red tape and move straight to the closing table. It’s a system that rewards progress over paperwork and leaves the stress of traditional approvals behind.

This guide shows you how to master the mechanics of private deals to get your deed without the bank. We’ll provide a clear understanding of the legal contracts and show you how to lower your barrier to entry. We break down the 2026 bank-free buying process into a simple, three-step sequence so you can claim your perfect parcel in record time. Get the facts, skip the bank, and start building your future today. It’s time to secure your land on your own terms.

Key Takeaways

- Cut the red tape and eliminate traditional lending hurdles. Learn how the seller acts as the bank to provide a direct, stress-free path to ownership.

- Master the mechanics of the deal. Understand how the promissory note and security instrument protect your investment without bank interference.

- Secure land with owner financing in days, not months. Save money by eliminating appraisal requirements and expensive origination fees.

- Access zero-commission listings directly. Use our specialized marketplace to connect with sellers and keep more cash in your pocket.

- Follow our simplified, bank-free buying sequence. Verify owners quickly and move from search to closing with total confidence.

What is Land with Owner Financing? The Bank-Free Path

Buying property doesn’t require a bank’s permission. In 2026, more buyers are choosing What is Land with Owner Financing? as their primary route to property ownership. This arrangement means the seller acts as the lender. You skip the loan officer and the 45-day underwriting wait. Instead, you and the seller agree on terms directly. You pay a down payment and make monthly installments until the balance is gone. This process creates “the note,” which is the legal document outlining your debt and payment schedule.

Institutional interest rates remained volatile through 2025, pushing land with owner financing into the mainstream. It’s a fast solution. You can often close a deal in 7 days or less. There are no 600-page applications. There are no hidden origination fees. You get the land you want without the red tape. By eliminating the middleman, you remove the biggest hurdle to closing. You deal with a person, not a corporate committee. This direct path provides a guaranteed way to secure acreage without the stress of traditional financing.

The process is simple. You find the property, agree on the price, and sign the paperwork. We focus on speed. We value your time. This method cuts out the commissions and the bank fees that usually drain your wallet. It’s the most efficient way to turn a dream of ownership into a recorded deed.

Who Benefits Most from Seller Financing?

Self-employed buyers with non-traditional income often struggle with bank audits. Owner financing ignores rigid debt-to-income ratios and focuses on your ability to pay. Investors also use this to preserve liquid capital for development. They put down a small percentage and keep their cash for clearing brush or building. It’s also the fastest route for buyers with a 600 credit score to build equity immediately.

The 2026 Landscape for Vacant Land

Raw land is the ideal asset for these structures because it lacks the maintenance risks of houses. In 2026, 42 percent of rural transactions now involve seller-carried debt. Buyers are moving away from 30-year institutional mortgages in favor of 5-year or 10-year flexible terms. During the payment period, the buyer holds “Equitable Title,” which is a legal interest that grants the buyer the right to obtain full legal title once the final payment is made. This ensures your investment is protected while you pay down the balance. It’s a transparent, reliable way to buy land with owner financing without the typical real estate headaches.

The Mechanics: How Owner Financing Works for Raw Land

Owner financing removes the bank from the equation. You deal directly with the seller to secure your property. This process relies on two primary legal documents. First, the Promissory Note acts as your legal promise to pay. It details the exact loan amount, the interest rate, and the repayment schedule. Second, the Security Instrument protects the seller by using the land as collateral. If you stop making payments, the seller has the right to take the land back through foreclosure or forfeiture. The Mechanics: How Owner Financing Works ensure that both parties stay protected throughout the life of the loan.

Repayment structures for land with owner financing are flexible. You aren’t stuck with a standard 30-year mortgage. Most deals use one of these three formats:

- Fixed-rate: You pay a set amount every month until the balance hits zero.

- Interest-only: Your monthly payments only cover the interest. You owe the full principal amount at the end of the term.

- Balloon payments: You make smaller monthly payments for a short period, typically 5 or 10 years, then pay the remaining balance in one lump sum.

Professional transactions always involve a third-party escrow company. They handle the money and ensure the deed is recorded correctly with the county. In 2026, digital escrow services have streamlined this, often cutting closing times to under 14 days. This setup prevents fraud and gives you peace of mind that your payments are being tracked accurately.

Land Contracts vs. Deeds of Trust

The legal structure of your deal changes who holds the title. In a Land Contract, or “Contract for Deed,” the seller keeps the legal title until you make the final payment. You hold “equitable title,” which gives you the right to use the land. A Deed of Trust is different. It transfers the legal title to you immediately. A neutral trustee holds the title in “trust” until you pay off the debt. For buyers in 2026, the Deed of Trust model is superior. It provides better legal protection and makes it easier to get building permits or utility connections early.

Negotiating the Terms of the Deal

You have the power to customize every part of the agreement. Start with the down payment. Most sellers look for 10% to 20% of the purchase price. If you offer a larger down payment, you can negotiate a lower interest rate. Aim for a rate that stays competitive; while traditional land loans often exceed 8%, owner-financed deals can sometimes land lower if you provide a strong down payment. Define your exit strategy by setting a clear balloon payment date. This gives you several years to improve the land or secure a traditional refinance. If you want a simple path to ownership, you can buy land directly from sellers who specialize in easy terms.

Owner Financing vs. Bank Loans: A 2026 Comparison

Traditional banks don’t like raw land. They view it as a speculative asset with no immediate cash flow. This bias makes getting a loan for vacant property a slow and painful process. Buying land with owner financing is the fastest path to deed transfer because it removes the middleman. You deal directly with the person who owns the title. This direct connection eliminates the red tape that stops most land deals before they start.

Banks rely on rigid algorithms to approve or deny your future. They demand high credit scores and perfect debt-to-income ratios. Sellers operate differently. They prioritize your down payment and your commitment to the property. Understanding Owner Financing: What It Is And How It Works helps you see why this method bypasses the rigid standards of 2026 institutional lenders. You gain the power to customize your terms; you can negotiate your interest rate, your payment schedule, and your balloon payments without a loan officer’s interference.

- Speed: Close in 7 days rather than 60 days.

- Cost: Zero loan origination fees and zero bank-mandated points.

- Flexibility: Create a payment plan that fits your seasonal income or business goals.

- Credit: Your handshake and your down payment matter more than a computer-generated score.

The Hidden Costs of Traditional Financing

Banks protect themselves by making you pay for their certainty. They often require a 50% down payment for raw land to offset their perceived risk. They also force you to pay for expensive third-party services you might not need. These include bank-mandated land surveys, environmental impact studies, and strict appraisal inspections that can cost thousands of dollars out of pocket. You can avoid these mandatory delays and expenses by focusing on owner financed land where the buyer and seller decide which tests are actually necessary for the transaction.

When to Choose Owner Financing

Choose owner financing when the property is in high demand and you cannot wait two months for a bank’s approval letter. This method is also ideal if you plan to build quickly. You can use the land as collateral for a future construction loan once you have established equity through your seller-financed payments. It provides a bridge to your ultimate goal without the initial hurdle of a mortgage application. While a standard bank loan for vacant property typically requires 45 to 60 days to close, an owner-financed transaction can be finalized in as little as 3 to 7 days. These flexible options for land with owner financing allow you to start your project now instead of waiting for a committee’s permission.

The Step-by-Step Guide to Buying Owner Financed Land

Buying land with owner financing skips the bank’s red tape. You deal directly with the seller. This process is faster, but you must follow a strict sequence to protect your money. Use this five-step checklist to move from browsing to owning.

- Find your parcel: Start on specialized platforms like BuyVacantLand.com. These marketplaces focus on sellers who already offer flexible terms. It’s more efficient than filtering through thousands of traditional listings.

- Verify ownership: Ask the seller for the current deed. Compare this against the county tax records. Ensure the person signing the contract actually has the legal right to sell the dirt.

- Perform due diligence: Investigate the physical and legal state of the land. Don’t skip this. You need to know what you can build before you sign any paperwork.

- Review the contract: Look for the interest rate, payment schedule, and any “balloon” payments. Professional review ensures there are no hidden fees or predatory clauses.

- Close and record: Sign the documents in front of a notary. File the contract with the county recorder’s office immediately. This makes your interest in the property a matter of public record.

Critical Due Diligence for Raw Land

Legal access is your first priority. Confirm the property has direct road frontage or a recorded easement. Without this, you could be landlocked and unable to reach your own property. Check the specific zoning codes with the county. Many rural areas have strict rules about RV living or minimum square footage for homes. If you are unsure about the process, read our guide on how do you buy land to understand the technical requirements. Verify utility availability; bringing power to a remote lot can cost over $10,000 depending on the distance to the nearest pole.

Protecting Your Investment

Always buy title insurance. This one-time fee protects you if a long-lost heir or an unpaid contractor claims ownership later. It’s a vital safety net for land with owner financing. Keep a meticulous paper trail. Use digital transfers or checks rather than cash so you can prove every payment. If you want to sell the land before paying it off, check your contract for a “due on sale” clause. This usually means you must settle your debt with the original seller before the new buyer takes over. Staying organized ensures you build equity without legal headaches.

Ready to start your journey? Browse our available land listings today and find your perfect property with zero bank hassles.

Finding Your Perfect Parcel on BuyVacantLand.com

BuyVacantLand.com is a specialized marketplace designed for action. We connect buyers and sellers without the interference of traditional brokers. Most real estate platforms focus on residential housing and suburban developments. They treat raw land like a secondary category, which makes your search difficult. We built this platform for one purpose: vacant land. Our system removes the noise so you can find exactly what you need.

Our model relies on zero-commission listings. You avoid the standard 6% to 10% agent fees that usually inflate land prices. This efficiency benefits everyone. Sellers offer better terms because they aren’t losing thousands of dollars to a middleman. You get a direct line to the decision-maker. It is the most pragmatic way to secure land with owner financing in the 2026 market. You deal with people, not institutions.

Finding these opportunities is simple. Our platform uses specific “Owner Financed” tags to highlight properties with flexible terms. You don’t have to guess if a seller offers a payment plan. The information is front and center. This transparency eliminates wasted phone calls and emails. You can see the down payment and monthly costs immediately. This allows you to make a decision based on hard facts. Our marketplace is built on these core advantages:

- Direct Communication: Speak directly to the person who owns the deed.

- Zero Commissions: Keep more of your money for the actual property.

- Verified Data: Access GPS coordinates and utility info without the fluff.

- Simple Search: Use filters designed specifically for raw and off-grid land.

The Power of a Targeted Marketplace

General real estate websites fail because they use house-centric filters. They don’t understand off-grid needs or agricultural zoning requirements. We’ve fixed that. Our discovery tool highlights properties based on their actual utility. Whether you want a hunting retreat or a homestead, our data is accurate. We simplify the search for cheap land for sale by removing the clutter found on big-box sites. You get the acreage and the direct contact info you need to move fast.

Ready to Start Your Search?

Start browsing our national database right now. We’ve listed thousands of acres across the country. Every listing includes a secure contact form. Reach out to the seller directly. Ask your questions. Get your answers. We’ve stripped away the corporate red tape. The process is fast, free, and guaranteed to be straightforward. You don’t need a bank’s permission to own property. Browse our current land with owner financing and take control of your future today. The parcel you want is waiting. Secure it before someone else does.

Secure Your Property Without the Bank

Traditional banks often make raw land purchases impossible with high down payments and strict 2026 lending standards. You don’t need to wait for a loan approval that might never come. By choosing land with owner financing, you bypass the red tape and deal directly with the source. This path offers a clear, three-step solution to property ownership that prioritizes your timeline over a bank’s schedule.

BuyVacantLand.com operates as a direct seller-to-buyer marketplace. We focus exclusively on vacant land parcels to ensure you get the most efficient experience possible. You’ll pay zero commission fees and zero hidden middleman costs during your transaction. Our platform removes the stress of traditional real estate by providing a fast, guaranteed way to secure your future acreage. The process is simple, transparent, and built for speed.

Stop letting high interest rates and bank bureaucracy stand in your way. Your ideal property is waiting for you right now. Browse Owner Financed Land Listings Now and start building your legacy on your own terms. It’s time to own the earth beneath your feet.

Frequently Asked Questions

Is owner financing safe for land buyers?

Owner financing is safe when you record the deed through a professional title company or a real estate attorney. According to the American Land Title Association, a recorded interest protects you against future claims or undisclosed liens. You must ensure the contract clearly defines the transfer of title. This transparency removes the risk of “clouded titles” that often stall traditional bank transactions.

Can I build on land that is owner financed?

You can typically build on the land if your contract specifically allows for property improvements. Most sellers require you to secure all necessary permits from the local county planning department before you break ground. Check your agreement for “prohibition of waste” clauses that might restrict land alteration. Building on the lot increases the property value and builds your equity faster.

What happens if I miss a payment in an owner financing deal?

Missing a payment triggers the default clause in your promissory note immediately. In a “Contract for Deed” structure, a seller may initiate a forfeiture process in as little as 30 days depending on your state’s specific statutes. In “Deed of Trust” states, the seller follows formal foreclosure procedures to reclaim the property. Always contact the seller to discuss a remedy before you lose your down payment.

Do I need a high credit score for owner financing?

You don’t need a high credit score because the land itself serves as the collateral for the loan. Sellers usually prioritize your down payment and proof of steady income over a traditional FICO score. Many private sellers skip the credit check process to keep the transaction fast and simple. This makes land with owner financing a reliable option for buyers with limited credit history.

How much down payment is typical for owner-financed land?

Expect to pay a down payment between 10% and 30% of the total purchase price. Data from the National Association of Realtors indicates that private sellers use these higher percentages to offset their financial risk. A 20% down payment is the standard benchmark for securing favorable interest rates. Higher upfront payments reduce your monthly costs and give you immediate equity in the dirt.

Who pays the property taxes in an owner financing agreement?

The buyer is responsible for property taxes in almost every owner financing agreement. You will pay the county assessor directly or contribute to an escrow account managed by the seller. Failing to pay these taxes can result in a tax lien, which typically violates your financing terms. Keeping these payments current ensures a clean title transfer once you pay the final installment.

Can I pay off the land early without penalties?

Most land with owner financing contracts allow you to pay off the balance early without any prepayment penalties. You should verify this by checking for a “Prepayment Penalty” clause in your promissory note before you sign. If no penalty exists, you can apply extra funds to the principal every month. This strategy cuts your interest costs significantly over a standard 5 to 10 year term.

Is a lawyer necessary for an owner-financed land purchase?

A lawyer is necessary to review the legal language and confirm that the seller actually holds a clear title. An attorney ensures the deed is recorded properly with the county recorder’s office to protect your legal rights. While you can close a deal without one, professional oversight prevents expensive legal disputes later. This small investment guarantees your path to ownership is fast, legal, and permanent.

Join The Discussion